Market Activity

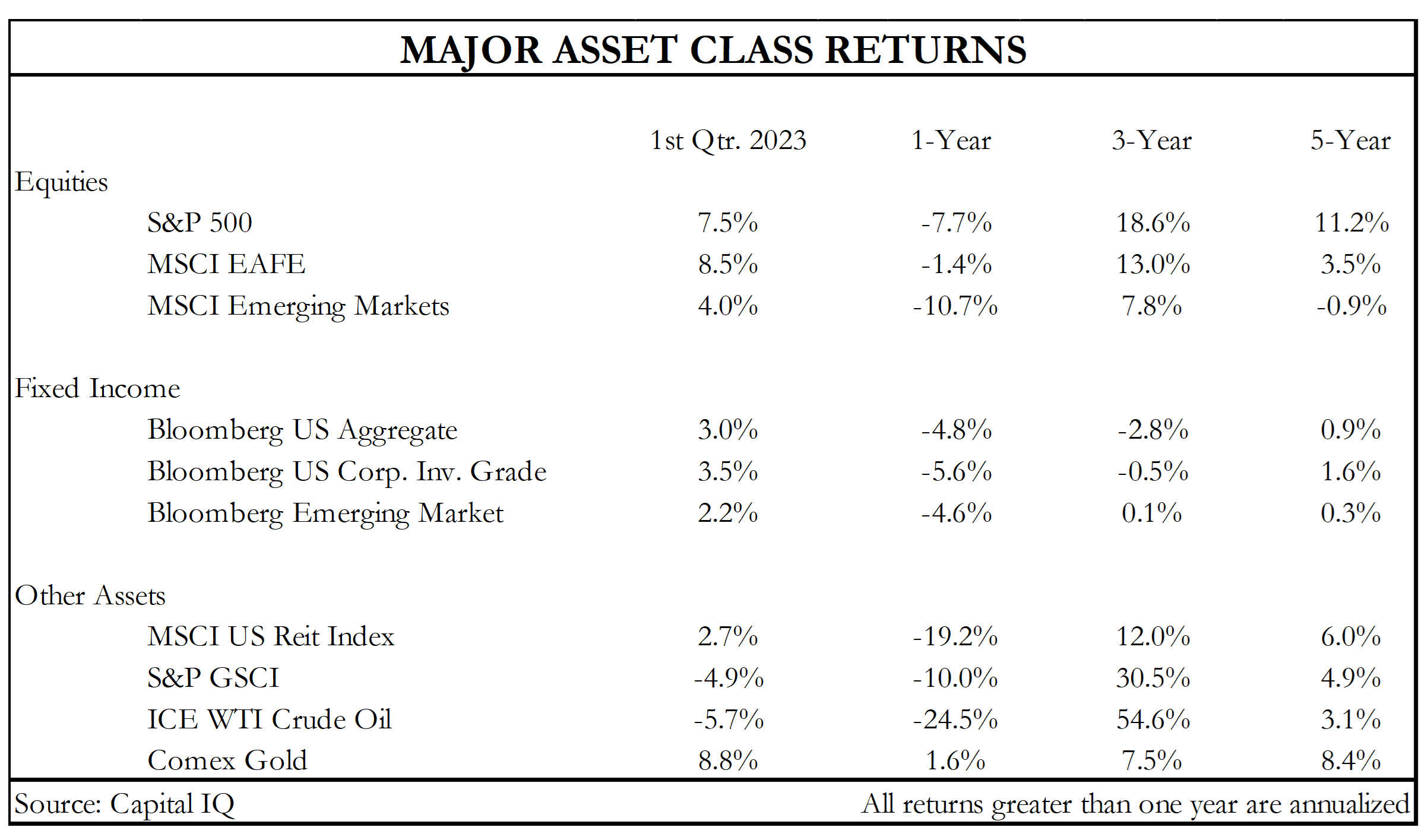

Equity and fixed income markets rebounded during the first quarter. The S&P 500 produced total returns of 7.5% as investors readjusted their expectations for short-term interest rates and some of the most beaten down securities in 2022 bounced. International developed markets also did well, as early 2023 economic data surprised to the upside and the U.S. dollar declined.

Fixed-income securities posted strong returns as interest rates across the yield curve declined, boosting security prices. The 2-Year U.S. Treasury tells the tale of the quarter. After ending 2022 at 4.43%, the 2-Year yield dropped to 4.09% by February 2nd, and then spiked to 5.07% on March 8th. Economic data both in the U.S. and around the world was better than anticipated, driving future Fed Funds expectations higher. After the debacle at Silicon Valley Bank (SVB), yields are lower across the curve, as investors now expect a much more muted Fed Funds rate path.

Click for Larger Image

Economic Activity

When judging the state of the global economy, it is important to consider the lag between the activity generating the data and the release of that data to the public or user. For instance, U.S. GDP data for the first quarter won’t be available until a month has passed (April 27th).

Better real-time indicators are the Purchasing Managers’ Indices, which measure business activity in both manufacturing and non-manufacturing sectors. Across the globe, these metrics improved during the first two months of 2023 when compared to the back half of 2022. The improving data was also much better than analysts were anticipating. For the U.S., this dynamic is best captured by the Citi Economic Surprise Index, which started 2023 in negative territory but has since moved decidedly positive.

Bank Failures

The collapse of Silicon Valley Bank and Signature Bank (together, S&S) rattled the financial markets amidst fears that it would cause a domino effect with negative impact on numerous banks. While we may see more bank failures in the months ahead, the problems will primarily be with small banks, who may lose deposits as people transfer to larger banks and institutions. To isolate S&S, it was encouraging to see government agencies and large banks quickly mobilize to prevent the problems from spreading.

While the S&S failures were driven by mismanagement and business models prone to deposit flight, some of the pressures on their business are impacting the entire banking system: deposit declines and higher interest rates. The pressures will likely continue to restrict credit, which in the U.S. is vital for economic growth. Credit growth has been slowing from the double-digit range during the first three quarters of 2022 to a more muted low single digit growth rate in recent months. While still early, weekly data is corroborating our expectations of S&S fallout, with loan growth declining and deposits continuing to shrink.

Click for Larger Image

Monetary Policy

Shifts in expectations for monetary policy were some of the wildest in recent memory. At the start of the year, the market for Fed Funds futures priced in a 13% chance that Fed Funds would be above 5.25% by June. By March 8th, this probability went to 99%. Today, it stands at 0%. The market is expecting close to 75 bps (0.75%) of cuts between June and the end of 2023.

Jerome Powell has suggested that he sees rate hikes and credit contraction from the banking crisis as one in the same. Our opinion is that credit will see a modest contraction with the Fed doing one, or possibly two more rate hikes of 25 basis points. From there, we expect Fed Funds to be held steady through the remainder of 2023, barring a significant economic slowdown.

Valuation & Sentiment

Looking at the S&P 500, valuations have become less attractive as the price has gone up and the earnings outlook has deteriorated. Analysts project S&P 500 earnings for 2023 of $221 per share, which would represent 1.2% growth from 2022. The Price to Earnings (P/E) multiple is a common yardstick that measures the price shareholders are paying relative to the cash flow (approximated by earnings) of the asset. Today, the S&P 500 P/E is trading in line with long-term averages.

From a sentiment perspective, individuals are bearish, which is a positive to us, as sentiment is a “contrary indicator”. A bearish outlook is corroborated by Goldman Sachs’ sentiment indicator, and fund flows exhibit a bearish tone as well.

Investment Outlook & Strategy

Interest rates and stock prices continue to be quite volatile, as stocks have traded in a range for the past two years. Though we know that stocks will eventually break-out of this pattern in a higher or lower direction, our guess/view favors higher (60/40 odds).

Though the media and economists continue to focus on (and predict) an upcoming recession, the economy continues to chug along and surprise the pessimists. From an investment perspective, the massive increase in interest rates in 2022, which caused a bear market in bonds and stocks, is now behind us. We can earn decent returns on bonds versus near zero for much of the past decade. Stocks are not cheap, nor are they excessively valued. Our view is stocks are fairly priced and offer attractive, long-term return potential relative to cash and bonds, albeit with higher levels of volatility. In brief, we continue to invest funds with normal assert allocations and a defensive bias.

Artificial Intelligence and Living with Constant Change

The economy and financial markets are constantly changing as they reflect what is transpiring throughout the globe. In future writings, we will share thoughts related to developments with AI (Artificial Intelligence), which is poised to change virtually all aspects of life.

In a recent talk, Microsoft Co-Founder Bill Gates expressed his view that Generative Artificial Intelligence will have an impact on life comparable to the development of the microprocessor, the personal computer, the internet, and the smartphone. As we all experience stress that change can often cause, we share the following words of wisdom …

“The more things change, the more they stay the same.” – Alphonse Karr

“What’s dangerous is not to evolve.” – Jeff Bezos

“The measure of intelligence is the ability to change.” – Albert Einstein

“If you can’t fly then run, if you can’t run then walk, if you can’t walk then crawl, but whatever you do, you have to keep moving forward.” – Martin Luther King Jr.

“All is flux, nothing stays still.” – Plato

“Times and conditions change so rapidly that we must keep our aim constantly focused on the future.” – Walt Disney

“The people who are crazy enough to think they can change the world are the ones who do.” – Steve Jobs

“It is not the strongest of the species that survive, nor the most intelligent, but the one most responsive to change.” – Charles Darwin

“Change is the law of life. And those who look only to the past and present are certain to miss the future.” – John F. Kennedy

The U.S. Debt Ceiling

Earlier this year, the U.S. government reached its debt ceiling, which is the legal limit on the total amount of federal debt. The money raised from borrowings is used to pay existing obligations, such as interest on Treasuries, Social Security benefits, Medicare, and military salaries. The U.S. is unlike many other countries in that they have laws enacted to limit the amount of debt it can have. The debt ceiling is most often quite contentious in Congress and the following overview provides a brief history.

Until World War I, Congress was required to approve each issuance of debt in separate legislation. Then in 1917, the Second Liberty Bond Act was enacted to simplify the process and enhance borrowing flexibility for issuance of government debt, eliminating the need for legislation each time. In 1939, Congress created the first aggregate debt limit, covering nearly all government debt, at $45 billion, which was 10% above total debt at the time. Fast forward and, since 1960, the debt limit has been raised, extended, or revised 78 separate times by Congress—49 times under Republican presidents and 29 times under Democrats. Currently, the government’s debt has grown to just under $31.5 Trillion. One important note: paying the debt is not about future spending. It is about meeting the cost of existing commitments the government has made.

Currently, Congress is back debating the debt limit as the limit enacted in 2021 was reached on January 19, 2023. Since then, Treasury Secretary Janet Yellen has taken “extraordinary measures” to prolong defaulting on any debt. It is estimated that the limits of reserves and other measures of meeting obligations will be reached in the third quarter of 2023. The extraordinary measures being employed by the Treasury Department were first utilized in 1985, and they have been used 6 times since May 2011.

We have seen this movie play out during these decades and they can be unnerving and impact financial markets. Yet, despite the back-and-forth bickering in Washington, we expect “better heads” to prevail. If the past is prologue for the future, the negotiating may continue until the last minute when time pressures force a compromised deal, as defaulting is not a viable option and would have global repercussions. The government’s obligation to pay its debts was written in the Constitution in the 14th amendment. Ultimately, those that govern our country will put emotions aside, practice the art of compromise, and negotiate with our country’s best interests ahead of their personal agendas.

We bring this to your attention as it will become more of a media focus as time marches on. Importantly, markets discount future events so the anxiety created by this logjam may be spread out over weeks. We are monitoring developments closely and will make appropriate adjustments, if needed and warranted.

Please view us as a resource for all your financial questions and needs, and as always, please contact us if we may be of assistance.

DISCLOSURES – This presentation is not an offer or a solicitation to buy or sell securities. The information contained in this presentation has been compiled from third party sources and is believed to be dependable; however, its accuracy is not guaranteed and should not be relied upon in any way whatsoever. This presentation may not be construed as investment advice and does not give investment recommendations. Any opinion included in this report constitutes the judgment of Lincoln Capital Corporation as of the date of this report and are subject to change without notice. Additional information, including management fees and expenses, is provided on Lincoln Capital Corporation’s Form ADV Part 2. As with any investment strategy, there is potential for profit as well as the possibility of loss. Lincoln Capital Corporation does not guarantee any minimum level of investment performance or the success of any portfolio or investment strategy. All investments involve risk (the amount of which may vary significantly) and investment recommendations will not always be profitable. The investment return and principal value of an investment will fluctuate so that an investor’s portfolio may be worth more or less than its original cost at any given time. The underlying holdings of any presented portfolio are not federally or FDIC-insured and are not deposits or obligations of, or guaranteed by, any financial institution. Past performance is not a guarantee of future results. Lincoln Capital Corporation prepare presentation, 401.454.3040, www.lincolncapitalcorp.com Copyright © 2026, by Lincoln Capital Corporation.